2023 Outlook for the farm equipment market

Tuesday, November 8, 2022

Reference: FCC

FCC Economics helps you make sense of the top economic trends and issues likely to affect your agri-business in 2023.

FCC Economics helps you make sense of the top economic trends and issues likely to affect your agri-business in 2023.Overall demand for farm equipment is projected to remain strong into 2023, despite rising interest rates and a weakening Canadian US exchange rate. Demand is supported by strong farm cash receipts, even with commodity prices softening from peak levels. As supply chains recover, equipment manufacturers are expected to increase the delivery of new equipment orders. However, inventory levels will remain below pre-pandemic levels as we project inventory levels could remain tight beyond 2024.

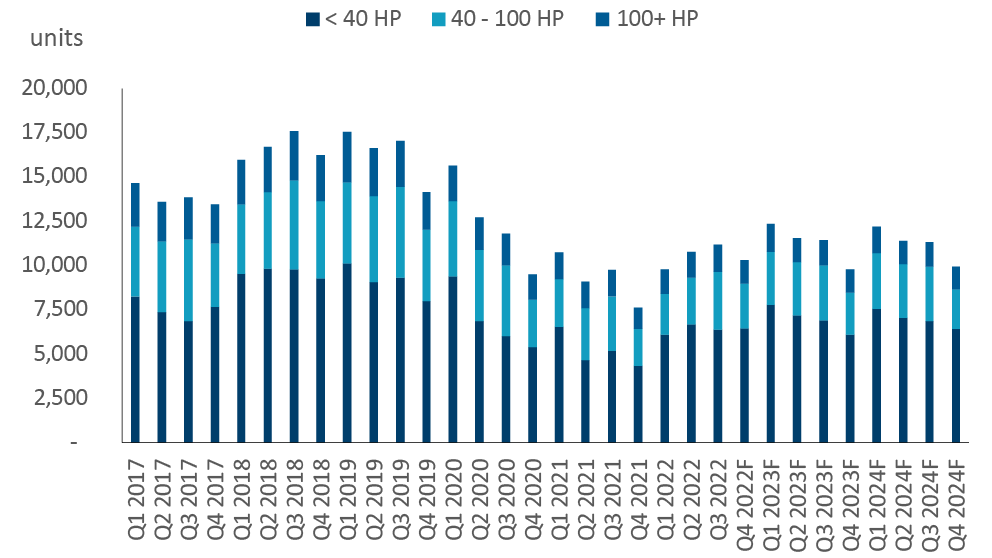

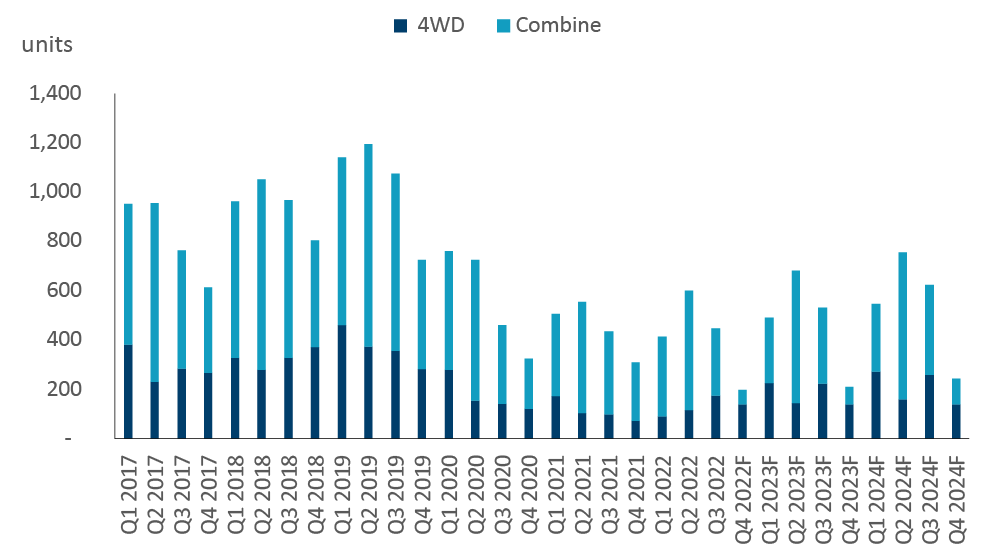

Sale projections

Sale trends for the remainder of 2022 are expected to be mixed. Higher horsepower tractors, combines, and implement sales are expected to have positive year-over-year growth, while lower horsepower tractor sales are expected to decline in 2022 because of slowing economic growth. Sales of smaller equipment are projected to decline as broad economic conditions worsen in Canada. A slowdown in low-horsepower tractor sales may allow manufacturers to allocate production to higher-horse-powered tractors utilized in agriculture. Further delays in equipment arrival before the end of the year could change these projections.Farm equipment sales projections for 2023 are projected higher for high horse-powered tractors, combines, and implement sales driven by strong crop receipts:

- 100+ HP tractor sales to rise 8.7%

- 4WD tractor sales to rise 13.9%

- Combine sales to rise 19.3%

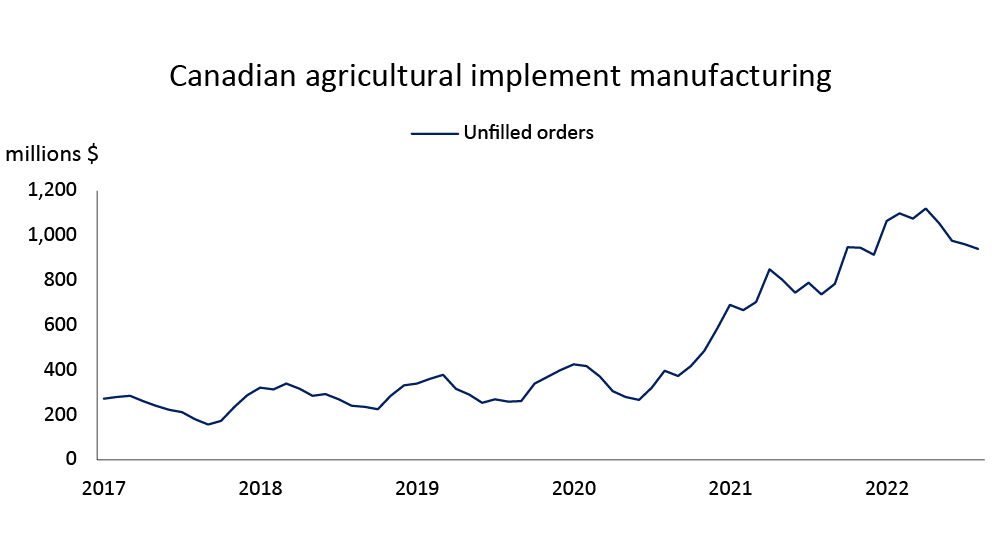

- Canadian agricultural implement manufacturing to rise 32.2%

- < 40 HP tractor sales to decline 0.4%

- 40 – 100 HP tractor sales to rise 0.4%

Figure 1. Supply chains are improving but are far from pre-pandemic levels

Source: Statistics Canada (NAICS 33311)

Inventory is projected to remain tight

We are anticipating inventory levels will remain tight through 2024 as producer demand remains strong for farm equipment and manufacturers catch up on pre-orders. Inventory levels of new farm equipment have trended below the five-year average (tractors are down 42% and combines down 47%). Strong demand for farm equipment for the remainder of 2022 is expected to reduce inventory levels further and support higher prices. The good news is that equipment manufacturers are expected to adjust their production upward due to the changing economic environment as North American equipment dealers begin to rebuild their inventories. We expect farm equipment dealers to remain 100% sold on new equipment. However, individual dealer revenue remains uncertain and tied to deliveries and allocations from manufacturers. Overall, dealer sale revenue will come down to the number of trades that materialize once new equipment arrives.- Combine inventory projected to remain pressured into 2024

- 4WD tractor inventory levels are projected to recover slowly

- Inventory levels are recovering for smaller horse-powered units